Excess Net Passive Income Tax Rate

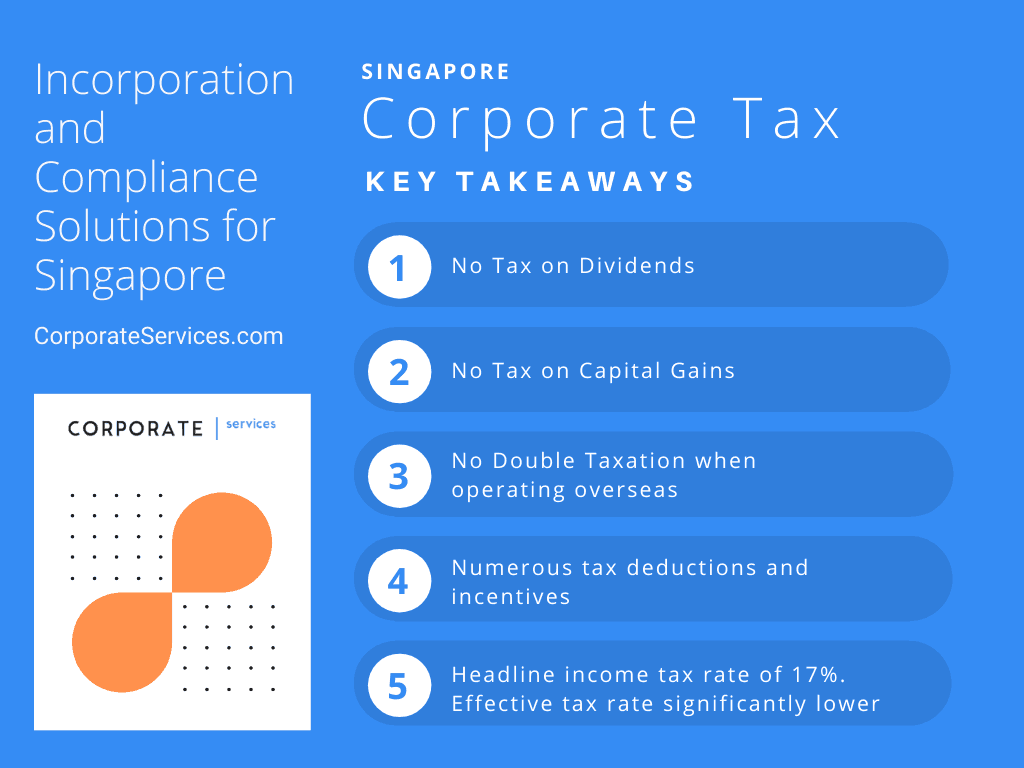

Singapore Corporate Tax 2020 Guide Taxable Income Tax Rates Incentives

The Rental Debt Snowball Plan How To Get Free Clear Rental Properties Debt Snowball Rental Property Investment Real Estate Investing Rental Property

How The New Tax Law Affects Rental Real Estate Owners Mitchell Wiggins

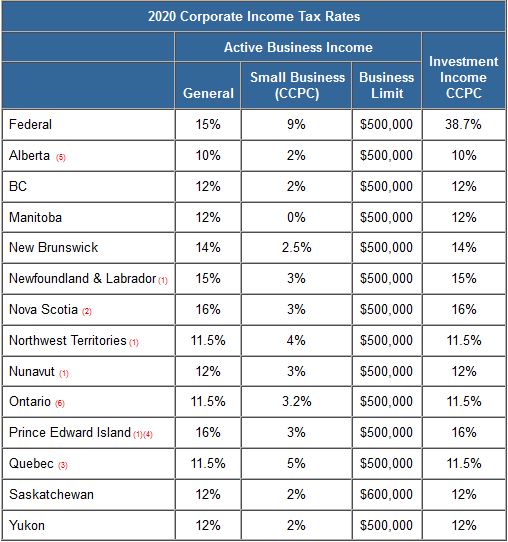

Taxtips Ca Business 2020 Corporate Income Tax Rates

Pin On Portfolio Tips And Investments

Simple Tax Guide For Americans In Vietnam

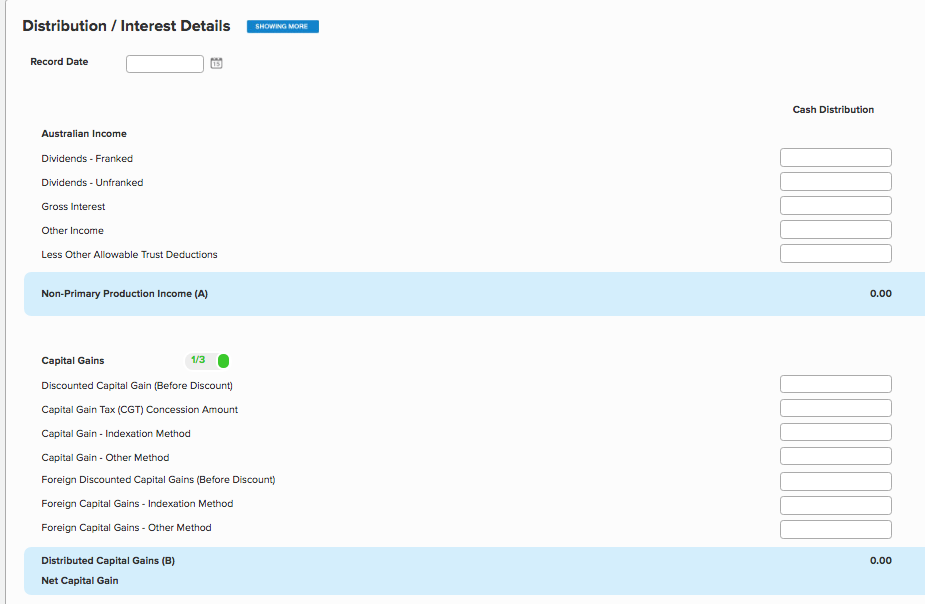

Imposed if an s corpora tion has accumulated earnings and profits at the end of the tax year and its passive investment income exceeds 25 of the corporation s gross receipts.

Excess net passive income tax rate. Excess net passive income is computed under a formula in which 1 the passive investment income in excess of 25 of gross receipts for the taxable year is divided by the corporation s passive investment income for the taxable year. Long term capital gains and qualified dividends are taxed at zero 15 and 20 percent for 2017 but the brackets are different. In the event the passive income exceeds 25 percent of the gross receipts of the corporation the excess net passive income tax comes into play. For purposes of this section 1 excess net passive income.

For 2017 passive income that is taxed as ordinary income will be taxed in the 2017 tax brackets and so the income tax rates range from 10 to 39 6 percent depending on your annual income. Excess net passive income tax excess net passive income is a corporate level tax on the passive income earned by an s corporation. The tax is assessed at the maximum corporate tax rate of 35. Tax shall be computed by multiplying the excess net passive income by the highest rate of tax specified in section 11 b irc sec.

There is an extra 1 18 percent marginal tax rate caused by pease limitations on all itemized deductions. However if it does have both e p and excess passive investment income some of the excess net passive investment income may be subject to tax at the highest corporate income tax rate currently 35 thus the sting. S corporations that have previously been a c corporation and have accumulated earnings and profits at the end of the tax year will be assessed a passive income tax if passive investment income for the year exceeds 25 of gross receipts for the year. And 2 the net passive income less deductions is multiplied by this percentage to arrive at excess net passive income.

Excess net passive income tax. Compute the annual income tax due. Except as provided in subparagraph b the term excess net passive income means an amount which bears the. The tax will not apply to a year in which there is no taxable income.

Corporate tax rate times excess net passive income. How much involvement an owner has in the s corporation will determine how much that owner will pay in taxes. Excess if any of the inventory. Passive income is derived from financial instruments that include.

S corporation owners are required to pay federal income taxes state taxes and local income tax. The excess net passive income tax applies if passive income is more than 25 of the s corporation s gross receipts.

Real Estate Or Stocks Which Is A Better Investment

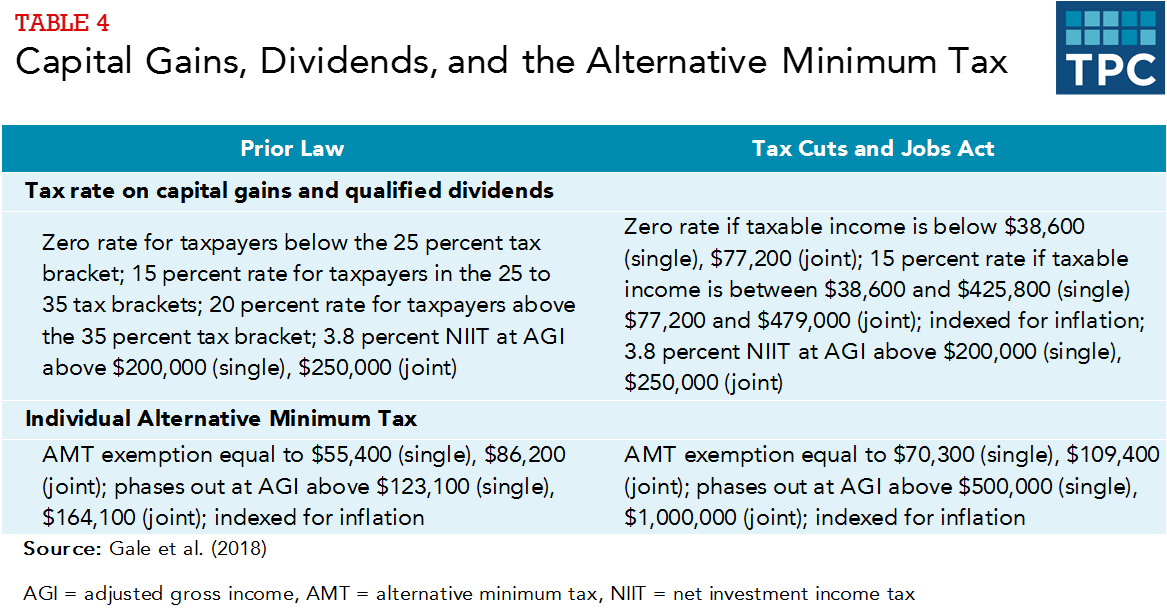

How Did The Tax Cuts And Jobs Act Change Personal Taxes Tax Policy Center

Tell Us Why The Flat Tax System Isn T Fair Because It Is

2 121 Likes 28 Comments Investing Entrepreneurship Entrepreneurmotivations On Instagram Str Money Management Advice Business Tax Deductions Investing

Our Retirement Investment Drawdown Strategy The Retirement Manifesto Investing For Retirement Investing Investment Accounts

At Risk Limits And Passive Activity Loss Income Tax Course Cpa Exam Regulation Tcja 2017 Youtube

Chapter 22 S Corporations Ppt Download

Https Www Irs Gov Pub Irs Pdf P1304 Pdf

Singapore Personal Income Tax Guide Guidemesingapore By Hawksford

I M 19 And Bought My First Car Cash The Wealthy Accountant Mr Money Mustache Finance Blog Money Saving Advice

Https Www Keystonecollects Com Forms Download Keystone 20guide 20for 20professional 20tax 20preparers Pdf

Publication 514 2019 Foreign Tax Credit For Individuals Internal Revenue Service

Net Investment Income Tax The Basics The H Group Portland Oregon